Inventory vs Marketplace : How India’s E-Commerce giants structure around FDI Regulations

In India’s fast-evolving e-commerce landscape, competition isn’t decided solely by logistics speed, pricing strategies, or customer experience – it is fundamentally engineered at the level of corporate structure. Beneath the surface of every “Add to Cart” click lies a carefully designed legal framework that determines who can sell, how inventory can be held, and even how profits flow. At the centre of this architecture is India’s Foreign Direct Investment (FDI) policy - less a passive regulation and more a strategic force that actively shapes how digital retail businesses are built and operated.

A closer look at inventory-based and marketplace models reveals how companies navigate these rules while balancing growth ambitions, control, and regulatory compliance in one of the world’s most dynamic consumer markets.

Understanding the Legal Divide

India permits 100% FDI under the automatic route in e-commerce, but this is subject to an important caveat; such investment is permitted only for entities operating under the marketplace model. Conversely, FDI is expressly prohibited in inventory-based e-commerce models.

Inventory-based model involves the entity purchasing, owning goods and selling them directly to customers. This resembles traditional retail and is ineligible for foreign investment in B2C e-commerce.

A marketplace model, on the other hand, acts as a facilitator between buyers and sellers. The entity here, provides the platform, facilitates payments, handles logistics and earns commissions for services provided by it. However, it does not take ownership of inventory during the process.

The rationale behind this distinction is clear - allowing foreign-funded entities to control inventory and pricing could enable deep discounting at scale, potentially undermining small domestic retailers that form the backbone of India’s retail ecosystem.

Further, the framework also has certain operational safeguards in place to ensure marketplace entities do not function as disguised inventory-led businesses:

- A seller’s inventory is deemed “controlled” by the marketplace entity if more than 25% of its purchases are sourced from that entity or its group companies.

- Sellers in which the marketplace entity (or its group companies) hold an equity stake, or exercise control, are barred from selling on that platform.

- Exclusivity arrangements between marketplaces and sellers are prohibited.

The above safeguards are closely tied to how “ownership” and “control” are assessed under India’s FDI policy.

FOCC vs IOCC: The Structural Backbone

In this context, entities are often classified as Foreign-Owned and Controlled Companies (FOCCs) or Indian-Owned and Controlled Companies (IOCCs). Marketplace entities with foreign investment are typically set up as FOCCs (often through wholly owned subsidiaries in India) and are therefore restricted from owning or controlling inventory or influencing vendors.

By contrast, entities classified as IOCCs, where ownership and control vest with Indian residents, eligibility to undertake inventory-based operations is not explicitly covered in the FDI Policy.

While the FDI policy focuses on sectoral restrictions, the Master Direction introduces a broader principle that “what cannot be done directly, shall not be done indirectly”. This implies that compliance extends beyond the immediate entity to the overall structure, including parent and subsidiary relationships.

In practice, policy considerations may extend to both the parent and its wholly-owned-subsidiary if the parent is classified as a FOCC. However, certain commercial arrangements have successfully mitigated this by structuring the parent as an IOCC, thereby enabling such models. Notably, this structure has been adopted without any regulatory challenges to date, which provides comfort in its continued viability.

In light of the above regulatory framework, let’s now take a look at the structuring arrangements of some of the most popular Indian E-commerce and Q-commerce businesses and how they’ve navigated through the regulatory requirements.

- 1. Snapdeal has remained a largely pure marketplace player, ensuring full FDI eligibility. Even when it briefly adopted a “controlled marketplace” model by introducing SD+ warehouses to gain operational control over logistics and delivery, not owning inventory ensured it remained FDI-compliant.

- 2. Blinkit presents a striking example of structural transformation. Initially constrained by foreign shareholding, it operated as a marketplace. However, in 2025, its parent entity Eternal Ltd. restructured to increase domestic ownership and qualify as an IOCC. This shift allowed Blinkit to adopt an inventory-led model-enabling tighter control over pricing, margins, and supply chains.

- 3. Amazon has consistently operated as a marketplace but previously relied on affiliated sellers such as Cloudtail and Appario to exert indirect influence over inventory and pricing. Regulatory tightening in 2018–19 forced Amazon to reduce these linkages, restructure seller relationships, and recalibrate its model to remain compliant.

- 4. Flipkart demonstrates a sophisticated dual-entity structure. Its wholesale arm “Flipkart India Pvt. Ltd.” procures inventory as a B2B entity, while its marketplace arm “Flipkart Internet Pvt. Ltd.” facilitates consumer sales without owning goods. This layered model allows it to maintain indirect influence over sourcing and pricing while technically adhering to FDI rules.

As seen from the above regulatory provisions and case studies, India’s FDI framework in e-commerce does more than impose restrictions. It actively determines how firms design their business structures.

It has also made it very clear that FDI eligibility depends primarily on ownership structure and legal classification rather than the degree of operational control exercised in practice.

Strategic structuring becomes not just a compliance requirement, but a key factor in maintaining competitiveness in the e-commerce sector.

Famous, reputed or well-known? Untying the knots in trademark law

Do you think if a trademark is considered to be well-known, it is a reputed mark as well? There is nothing wrong in assuming the terms to be synonymous if you do not belong to the legal fraternity. But in the legal parlance, there is a very delicate line of difference between the two phrases. In other words, we could say that “every famous brand is reputed, but not every reputed mark is legally ‘well-known’.” In this article, we will break down the use of these phrases and put them in proper perspective for the benefit of the non-lawyers.

Let us consider a scenario where your mom is looking for a groom for you, and she says she has registered your profile in the ‘Gucci matrimony.’ On hearing, you are astonished and instantly think, when did Gucci start their matrimony services. Even though Gucci has nothing to do with the local matrimony site, the mark is so universally recognized that even the common man can relate the service with Gucci in less than a second. This is what the law addresses as a “well-known mark.”

Meanwhile your father brings you sizzling hot onion pakoras from one of the best tea shops in town called the ‘Iyengar Delight’ which serves hot tea and snacks. Everyone in the city recognizes it, but only a very few from outside the city will know it. This shows that the brand has extreme reputation and strong goodwill only within that locality. This differentiates a “well-known mark” from a “mark with reputation.”

Where does the law actually stand?

The trademark law posits certain grounds under Section 11(6) of the Trade Marks Act, 1999 (“Act”), for a mark to be considered as a “well-known mark”, viz.,

- the acknowledgment the mark has gained amongst the ‘relevant sector of the public’;

- the proof of duration for which the mark is “well-known” and the geographical area where the mark is of use or being promoted or advertised;

- the proof of when and where it is registered or any application has been filed for registration under the Act; and,

- the record of successful enforcement rights by which the trademark has been recognized as a well-known mark by any court or registrar.

On the other hand, Section 29 of the Act speaks about infringement and Section 29(4)(c) stipulates the conditions for a ‘mark with reputation’, that is, the registered trademark has a reputation in India, and the use of the mark without due cause takes unfair advantage of the reputation of the registered trademark. Thus, a mark with reputation is nothing but a criterion to satisfy infringement and does not possess any other additional privileges

In conclusion, a “well-known mark” is where the holder of the mark can initiate a suit for infringement and has an additional privilege of preventing registration of the trademark under any class of goods or services, but a ‘mark with reputation’ is something which is only a prerequisite for infringement.

The Delhi High Court tried to clarify this confusion in Bloomberg Finance Lp V. Prafull Saklecha & Ors., CS (OS) No.2963 of 2012 by establishing that if a trademark is legally recognised as well-known, this status fills the ‘reputation rule’ under Section 29. Likewise, in RPG Enterprises Ltd v. Riju Ghoshal.,2022 SCC OnLine Bom 626, the Court laid down that the words ‘well-known mark’ and ‘mark with reputation’ cannot be used interchangeably as they fulfil two different purposes under the Act. Yet another point to be taken note of is the local reputation criterion. If the intent of Section 29 is looked at, the mark requires reputation in India, but no such condition can be found in Section 11.

- A reputed trademark is a mark that has goodwill and recognition among a particular set of population or local reputation, while a well- known mark enjoys broader public recognition, may be even transborder reputation.

- Every well-known mark is reputed, but not every reputed mark is legally recognised as “well-known.”

- Well known trademarks get a special privilege of preventing others from using it for unrelated goods and services because the consumers will be able to relate it to the original brand.

- The phrases cannot be used interchangeably as each of it has its own purpose reiterating the intent of law.

Down Rounds in Indian Startups: Valuation Reset and Investor Dilution

Every startup story celebrates the up-round — a higher valuation, more investor confidence, headlines. But what happens when the next round comes in lower than the last? That is called as a down round. And in India's startup ecosystem, they are no longer rare events.

1. What Is a Down Round?

A down round occurs when a company raises fresh capital at a valuation lower than its previous funding round. In simple terms, the company is now valued less on paper than it was before.

This can happen for several reasons such as weaker than expected business performance, a shift in market sentiment, tighter investor scrutiny on unit economics, or regulatory risks. In India, the funding benchmarks of 2022-23 triggered several high-profile down rounds, bringing valuations that had surged during the 2021 boom period sharply back to earth.

2. How Valuation Is Reset in a Down Round

The new valuation in a down round is typically negotiated commercially between the company and incoming investors, based on current business fundamentals - revenue, burn rate, growth trajectory, and comparable market transactions.

Valuation methodologies used include:

- Income Approach (DCF) - revised with more conservative growth assumptions and higher discount rates reflecting increased risk

- Market Approach - recalibrated against current trading multiples of comparable companies, which may have contracted significantly

- Recent Transaction Approach - benchmarked against similar funding rounds in similar-stage companies

The reset valuation determines the price per share at which new investors come in — and this lower price is the trigger for anti-dilution protection mechanisms for existing investors.

3. Investor Dilution — Who Bears the Pain?

Dilution in a down round is not felt equally. Its impact depends on the type of shares held and other terms in the shareholders agreement.

Founders typically bear the most dilution. They hold common equity with no downside protection. A lower valuation combined with a larger share issuance to new investors and potential conversion adjustments for existing investors can significantly erode their ownership percentage.

Early-stage investors without anti-dilution protection face the same fate as founders, their percentage stake shrinks without any compensatory adjustment.

Investors with anti-dilution protection are partially shielded. The practical effect of anti-dilution clauses is that the dilution burden shifts — away from protected investors and onto founders, early stage investors and employees holding ESOPs.

4. Key Considerations Before and During a Down Round

Companies navigating a down round should address the following before closing the transaction:

- Review all existing investor agreements for anti-dilution clauses, consent rights, and pre-emptive rights — these may require formal waivers before new shares can be issued

- Obtain a fresh independent valuation to support the new price - this is essential for regulatory compliance and for defending the pricing to existing shareholders

- Assess accounting reclassification risk - review whether any convertible instruments or preference shares need to be reclassified following the reset

- Communicate proactively with ESOP holders - a down round resets FMV and affects the value of unvested and vested options; timely communication avoids disputes

- Board and shareholder approvals - fresh issuance of shares requires board approval and, in most cases, a special resolution from shareholders under the Companies Act

5. Conclusion

Down rounds are a structural feature of startup ecosystems — not an anomaly. In India, where valuations ran ahead of fundamentals through much of 2020-21, corrections were inevitable. The companies that navigate down rounds well are those that plan for them with robust shareholder agreements, clean cap table documentation, independent valuations, and transparent communication. A down round need not define a company's trajectory. But how it is managed almost always does.

A down round is as much a governance event as it is a financial one. The valuation reset is just the headline, beneath it lies a chain of legal, accounting, tax, and stakeholder obligations that demand careful execution. For founders, the lesson is to negotiate anti-dilution terms thoughtfully at every round, not just when things look uncertain. For investors, it is a reminder that paper markups are not returns. And for the ecosystem at large, down rounds are a necessary correction mechanism that, when handled well, restore credibility and set the stage for sustainable growth.

Family business preservation

Tax, Structuring & Regulatory Perspectives

Family-owned businesses account for a dominant share of India's private sector output and employment. Yet transferring family wealth and business control across generations remains fraught with legal complexity, tax exposure, and regulatory risk. A structured approach — addressing entity design, tax planning, and compliance architecture — is essential for business continuity and wealth preservation. These challenges are not unique to India; family enterprises globally navigate similar tensions between control, tax efficiency, and governance.

1. Family Business Structure Mechanisms — Indian & Global Perspective

The table below maps the key structuring vehicles available to family businesses, drawing from both Indian law and global practice, along with the core tax and regulatory considerations for each:

| Structure | Indian Context | Global Equivalent | Tax & Regulatory Highligh |

|---|---|---|---|

| Private Limited Company / Corporation | Pvt. Ltd. under Companies Act 2013; DVRs & Article-based transfer restrictions keep ownership within family | S-Corp / C-Corp (USA); GmbH (Germany); SAS (France); Pte Ltd (Singapore) | Dividend Distribution Tax removed (w.e.f. FY21); LTCG on unlisted shares at 12.5% without indexation; Companies Act governs buybacks & RPTs |

| Hindu Undivided Family (HUF) | Unique to India; treated as separate taxable entity under IT Act 1961; own exemption slab & deductions | No direct global equivalent; loosely analogous to Family Partnership in civil law countries | Income taxed at individual slab rates; HUF partition tax-neutral u/s 171 IT Act; Clubbing provisions apply on transfers to spouse / minor children |

| Discretionary / Specific Trust | Indian Trusts Act 1882; assets outside personal estate of settlor; protection from creditors & matrimonial claims | Revocable / Irrevocable Trusts (USA, UK); Jersey / Cayman STAR Trusts; Liechtenstein Foundation | Trust income taxed at Maximum Marginal Rate (30%+) unless specific beneficiary; offshore trusts governed by FEMA/LRS; PMLA UBO disclosure mandatory |

| Holding Company Architecture | Holding Company holds operating subsidiaries; ring-fences risk; centralises family treasury | Holding Company (Netherlands BV; UK Holdco; Singapore Pte Ltd) — used globally for IP holding & treasury | Dividend income exempt u/s 10(34) on domestic dividends (post-DDT repeal, dividend taxable in hands of shareholder); CCI approval required if M&A thresholds crossed |

| LLP / Family Limited Partnership | LLP Agreement governs profit-sharing, admission & exit; suited for investment / professional family firms | Family Limited Partnership (FLP) — USA; Commandite (France/Belgium); KG (Germany) | LLP income taxed at 30% (flat); no DDT-equivalent; valuation discounts available on FLPs in US estate planning |

| Family Foundation | No standalone Indian foundation law; structured via Section 8 Company or Public Charitable Trust | Stiftung (Germany/Austria); Family Foundation (Liechtenstein, Malta); Fondation (Luxembourg) | Section 8 Company exempt u/s 11-13 IT Act if applied for charitable purposes; foreign contributions governed by FCRA; offshore foundations may trigger FEMA filing obligations |

| Family Office Structure | Multi-Family Office (MFO) or Single-Family Office (SFO) as Pvt. Ltd. or LLP; SEBI registered if managing third-party funds | SFO / MFO globally (Switzerland, Singapore, UAE); SEBI AIF / PMS licence needed for pooled management | SFO income (management fees, investment income) taxable; SEBI registration mandatory for external AUM; FEMA compliance for offshore SFOs; FATCA / CRS reporting for cross-border families |

2. Tax-Efficient Wealth Transfer

India does not levy estate duty or inheritance tax (abolished 1985), but several provisions require careful navigation:

- Gift Tax: Gifts between specified relatives are fully exempt u/s 56(2) IT Act; gifts to non-relatives exceeding INR 50,000 in aggregate are taxable as income in the recipient's hands.

- Capital Gains: LTCG on unlisted shares at 12.5% without indexation (held 24+ months); transfers on death do not attract capital gains — tax crystallises only on the heir's sale.

- Stamp Duty: State-specific stamp duty applies on property and, in some states, unlisted share transfers; many states offer concessional rates on intra-family transfers.

- Offshore & DTAA: Families with cross-border interests must structure offshore holdings through DTAA-favourable jurisdictions; FEMA/LRS governs outbound fund flows; FATCA/CRS compliance is mandatory for globally mobile families.

3. Regulatory Framework for Succession

- Companies Act: Companies Act 2013 governs share transfers, buybacks, and RPTs; buy-sell provisions in Shareholder Agreements must align with the Articles to be enforceable.

- SEBI: SEBI Regulations impose additional obligations on listed promoter families — reclassification, pledge disclosures, and insider trading restrictions all intersect with succession events.

- Succession Laws: Hindu Succession Act 1956 (amended 2005) gave daughters equal coparcenary rights in HUF property — a material change for estate planning. A registered Will and Trust deed override intestate outcomes.

- PMLA & UBO: Trusts and holding structures must comply with PMLA beneficial ownership (UBO) disclosure requirements under both the Companies Act and SEBI KYC norms.

- Competition Law: Family restructurings involving mergers, demergers, or amalgamations above prescribed thresholds require CCI approval under the Competition Act 2002.

4. Structuring for Business Continuity

- Separate ownership from management — use trust/holding structures for ownership and a professional Board for operations

- Adopt a comprehensive Shareholder Agreement covering valuation methodology, drag-along/tag-along rights, and compulsory transfer on death or divorce

- Review Wills and Trust deeds every 3–5 years and after every major life or business event

- Conduct a periodic 'succession tax audit' to identify latent capital gains, stamp duty, and gift tax exposures

- Consider pre-IPO restructuring to simplify holding structures, eliminate inter-corporate loans, and clean up related-party transactions

Preserving family business wealth across generations is a multidisciplinary exercise — combining legal structuring, tax optimisation, regulatory compliance, and governance design. Whether through an Indian HUF and discretionary trust, or a Singapore holding company and Liechtenstein foundation, the principles are universal: separate ownership from control, plan transfers proactively, and ensure compliance at every layer. In India's rapidly evolving regulatory landscape, families that treat succession as a long-term, professionally managed project — not a reactive, crisis-driven event — are best positioned to endure.

ESOP Valuations: Key Tax & Accounting Considerations

ESOPs are no longer just a retention tool — they are a financial instrument that sits at the intersection of tax, accounting, and legal compliance. Yet in practice, many companies treat ESOP valuation as an afterthought - a box to tick before a board meeting. That approach carries real risk. So why does ESOP valuation matter in the first place?

Simply put, every time an employee exercises an option, a taxable event is created. The quantum of that tax and the expense the company must recognise in its books, both depend on one number: the Fair Market Value (FMV) that can be associated with the ESOPs. An incorrect or poorly documented FMV can trigger tax and accounting implications. Hence, getting it right is not optional.

1. Why Valuation Is Required — and What It Drives

ESOP valuation serves two distinct but equally important purposes.

For tax purposes, FMV on the date of exercise determines the perquisite value in the hands of the employee and therefore the TDS the company must deduct and deposit. It also becomes the employee's cost of acquisition for capital gains when shares are eventually sold.

For accounting purposes, the fair value of the option at the date of grant determines the ESOP expense that the company must recognise in its P&L over the vesting period under the accounting standards.

These are two separate valuation exercises, governed by different frameworks, requiring different methodologies and often confused as one. Keeping them distinct is the first step to getting ESOP compliance right.

2. Valuation Methodology

The choice of methodology must be appropriate and internationally accepted. Internationally accepted methodologies commonly applied include:

- Income Approach

- Market Approach

- Asset Approach

- Option Pricing Models

The methodology selected must be well-documented, consistently applied across reporting periods, and defensible under regulatory scrutiny.

3. Point of Taxation — A Two-Stage Reality

ESOPs are taxed at two distinct stages, and the company carries compliance obligations at both.

Stage 1 — On Exercise (Perquisite Tax): The spread between FMV on the date of exercise and the exercise price is treated as a perquisite and taxed as salary income. The employer is required to deduct TDS and deposit it to the government on behalf of the employees, it’s similar to salary taxation.

Example: FMV = ₹600/share, Exercise Price = ₹50/share → Taxable perquisite = ₹550/share, taxed at the employee's applicable slab rate.

Stage 2 — On Sale (Capital Gains Tax): When shares are eventually sold, capital gains tax applies on the difference between the sale price and the FMV on the date of exercise, which becomes the employee's cost of acquisition.

4. Accounting Impact — The Hidden P&L Charge

ESOPs are not off-balance-sheet item. Under the accounting standards, companies must Fair Value the option as on the date of grant and recognise the expense component in the books, spread over the vesting period. This is a non-cash charge, but it directly reduces reported EBITDA and profit after tax, and must be disclosed in the financial statements with full supporting assumptions.

The inputs to the option pricing model like expected volatility, risk-free rate, dividend yield, expected option life etc. must be consistent, documented, and reviewed each reporting period. Errors in these computations are among the more common causes of financial restatements in high-growth companies and attract heightened scrutiny from auditors.

5. Key Considerations Before Audit Finalisation

Before closing the books, companies should run through a structured ESOP checklist covering the following:

- Grant date fair value: Has the fair value of all options granted during the year been computed using an appropriate internationally accepted methodology, with clearly documented assumptions?

- Expense computation: Has the ESOP charge been correctly calculated, accounting for new grants, forfeitures, cancellations, lapses, and any modifications made during the year?

- Vesting schedule accuracy: Are service conditions and performance conditions correctly tracked, and do they align with the expense recognition pattern applied in the books?

- Disclosure adequacy: Do the financial statement notes adequately disclose option movements, remaining contractual life, and the key assumptions used in fair value computation?

6. Conclusion

ESOP valuation is an ongoing financial discipline — not a one-time compliance event. It touches tax and accounting compliance in equal measure, and gaps in any one area can lead to issues at the time of audit or regulatory reviews. What often goes wrong is not ignorance of these rules, but the absence of a structured process to apply them consistently across every grant cycle and exercise event.

For companies serious about building credible ESOP programmes, the foundation is simple: the right valuation professional at the right stage, a well-documented methodology, and internal processes that treat ESOP compliance as a finance function, not an afterthought.

Exports Under FEMA : What you really need to know

Shipping the goods and raising the invoice are only the first steps. Under India's foreign exchange framework, an export transaction remains open until the proceeds are repatriated through an AD bank and the underlying reporting is formally closed. A write-off in your accounts does not satisfy this requirement — that distinction is where most compliance exposure originates.

1. The Timelines That Actually Matter

The RBI updated repatriation timelines in November 2025, and they are now more realistic for how cross-border trade actually works. Here is what is in effect:

- Goods exports: 15 months from shipment date

- Service exports: 15 months from invoice date

- Warehouse exports: 15 months from date of sale

- INR-denominated exports: 18 months from invoice or transaction date

- Advance payment shipment window: 3 years from date of advance receipt (previously 1 year)

If you are still working off the old nine-month rule, that has been superseded. The extension reflects ground-level commercial reality: disputes happen, logistics get complicated, and overseas buyers do not always pay on schedule.

Longer timelines do not mean lower scrutiny. RBI still expects you to either collect within the window or have a documented, bank-supported explanation for why you did not.

2. When You Need More Time: Filing Form ETX

Form ETX and the Formal Extension Route

When collection delays exceed what your AD Category-I bank can approve under its own delegated authority, the matter moves to RBI through a formal application — Form ETX, submitted in duplicate via your AD bank.

What to submit alongside the form:

- Invoice-wise and shipping-bill-wise statement of all unrealised export dues

- Original buyer or correspondent bank correspondence documenting follow-up history and reasons for non-payment

- Bank evidence of any partial realisations received against the outstanding invoice

- Settlement agreements or legal records, where proceedings have been initiated

- A CA-certified schedule, if your AD bank requires it prior to forwarding the application to RBI

Practical Tips

Banks respond very differently to a well-organised, proactive extension request versus a retrospective one filed under pressure. The moment an invoice begins ageing — not when the deadline is in sight — is the right time to start building the documentation file. Correspondence logs, follow-up emails, buyer acknowledgements, and any partial payment records should be collated as they happen rather than reconstructed later.

3. Write-Offs: Not Just an Accounting Entry

Under FEMA, a write-off is not a unilateral commercial decision. It is a regulated closure. You are formally notifying the bank and potentially the RBI that a receivable is uncollectable and requesting the export entry be cleaned up accordingly.

The Three-Tier Structure

Write-offs operate within a hierarchy based on who has authority to approve:

- Self write-off by the exporter (within RBI-prescribed limits)

- Write-off by the AD Category-I bank (within its delegated powers)

- RBI approval required when amounts exceed the above limits

The Headline Limits

| Category | Limit | Basis |

|---|---|---|

| Self write-off (general exporter) | 5% | Total export proceeds realised in the previous calendar year preceding the year in which the write-off is being done |

| Self write-off (Status Holder Exporter) | 10% | Same as above |

| AD Category-I Bank write-off | 10% | Same as above |

These limits are cumulative across the year, not per transaction. Once you exceed your self write-off threshold, the AD bank must process it or escalate to RBI. Repeated breaches or weak documentation can cause banks to withdraw the self write-off facility entirely.

Timing Threshold

Write-offs within these limits are generally only available where the export receivable has been outstanding for more than one year, subject to specific RBI conditions. Confirm the applicable criteria with your AD bank before initiating.

What Documentation Actually Gets Scrutinised

This is where most write-off applications succeed or fail. Banks look for genuine evidence of collection failure:

- Insolvency or bankruptcy records for the overseas buyer

- Evidence of goods destroyed, seized, or auctioned abroad

- Legal confirmation of impossibility of recovery

- Documented commercial dispute with a resolution trail

For self write-offs, a CA certificate is commonly required: covering invoice details, prior write-offs taken in the year, and confirmation that export incentives have been dealt with as required by policy.

One Important Nuance on ECGC Claims

When ECGC or another IRDAI-regulated insurer settles a claim, the AD bank can write off the related export bill based on the insurer's confirmation, and this category is typically not constrained by the standard 10% limit. However, claims settled in INR are not treated as foreign exchange realisation. This matters for export incentive eligibility and downstream compliance outcomes, so factor it in before you proceed.

It is important to treat export receivables as compliance items, not just treasury items.

Here is what that looks like in practice:

- Start a file for every export invoice from day one: reminders sent, buyer replies, dispute notes, partial receipts, and your intended resolution path

- Do not wait for timelines to lapse. Loop in your AD bank early if collection looks uncertain

- Know which approval bucket you are in: self write-off within limits, AD bank write-off, or RBI escalation. The documentation you need differs significantly across each

- If export incentives such as IGST refunds or duty drawback were claimed, understand what happens to them on write-off. Recovery requirements may apply

For advisors, the question your clients need answered is not just whether they got paid. It is whether the transaction can survive scrutiny when they did not

Leave Encashment and Carry Forward: What HR’s must Know

The one question that lingers and haunts HR’s of every company is “Leave encashment” and “Carry forward of leaves”. Should we allow encashment of earned leaves as a part of full and final settlement? What are the maximum leaves that can be carried forward? Are these mandatory under any law? To clear the fog around, this article aims to discuss these issues vis-à-vis Karnataka Shops and Commercial Establishment Act, 1961(“Act” for brevity) and the Labour Codes.

What does the law state?

Section 15 of the Act provides for both encashment of leaves and carry forward of leave

- Carry Forward of leaves

- When an employee does not avail themselves of earned leaves (viz one day for every 20 days of work or as mentioned in the Company’s Policy) allowed to them in a year, then such leaves are allowed to be carried forward to next year.

- Maximum unused earned leaves that can be carried forward is up to 45 days.

- When the Employer denies the earned leaves applied for, then such employee will be entitled to unlimited carry forward of leaves.

- No other form of leave, other than earned leave such as sick leave shall be eligible to be carried forward.

- Leave Encashment

- As per section 15(13) of the Act leaves can be encashed in the following situations:

- Termination of employment before the employee availed the leaves; or

- Leave having been denied, the employee quits before taking such leave.

- Encashed leaves must be paid at a rate equal to daily average of total full-time earnings excluding any overtime or bonus.

- Leaves should be encashed within 2 days where the employer has terminated the employee. In case where the employee quits, then on or before the next pay day.

- It is important to note that the Act is silent about encashment of leaves:

- during the employment; or,

- when the employee resigns.

- The law is also silent if the carried forward leaves must be encashed once it exceeds the threshold of 45 days and remains unused.

Analysis

The common question asked around “carry forward” is if less than 45 days of leaves can be carried forward. The law states that the maximum number of leaves that can be carried forward is 45 days. This would lead to two interpretations, i.e., since the law does not prescribe a lower limit, the Company could deny carry forward of leave or alternatively allow up to 45 days of leave to be carried forward. In relation to labor and employment matters, it is now res integra that whenever there are two or more interpretations possible, then the most beneficial interpretation must be adopted (Lalappa Lingappa and Ors. v. Lakshmi Vishnu Textile Mills Ltd. (Civil Appeal No. 930 of 1980). Therefore, in our opinion, carry forward of up to 45 days of leave will be preferred by the executive and judicial authorities.

With regards to encashment of leaves, the law is silent about encashment during employment as well as resignation under normal circumstance. Hence, it may be left to the discretion of the employer whether to grant leave encashment or not.

Encashment and carry forward through the Lens of Labour Codes:

These topics have been made abundantly clear under section 32 of the Occupational Safety and Health and Working Conditions Code, 2020(“OSHW Code” for brevity). It provides for the following:

- Section 32(vii) of the OSHW Code allows for carry forward of leaves up to 30 days of unutilized leave. If any leave applied to and is refused, such leave can be carried forward without any limitation.

- As per Section 32 of the OSHW Code, leave encashment is allowed on the happening of any of the following events –

- discharge or dismissal or termination

- resignation

- superannuation

- death during the course of calendar year

- at the end of calendar year, on demand of employee

- when the carried forward leaves exceeds 30 days, excess leaves shall be encashed

- Leaves must be encashed within 2 working days from the date of discharge, dismissal or quitting and within 2 months in cases of superannuation or death.

Under the new labour codes, given that the leaves can be encashed at the end of each calendar year on demand, it is discretion of the Employer to limit carry forward of leaves to anywhere between 0-30 days. Employers must consider factors like employee well-being, business continuity, financial liability and other such factors while deciding this threshold.

Though provisions related to leave encashment and carry forward have been made abundantly clear now, these provisions under the new labour codes apply to all employees except those employees in managerial, administrative or supervisory capacity/role earning wage more than Rs. 18,000. Per contra, that is to say that for such exempted employees the Karnataka Shops and Commercial Establishments Act, 1961 continues to apply.

Conclusion

Leave encashment and carry forward of leaves are often areas of uncertainty for employers, particularly due to gaps in drafting of the statutes. Under the Act, section 15 is silent regarding the encashment of leave when employee resigns and carry forward of leaves is a question of interpretation. However, these gaps in drafting and interpretations are put to an end in the OSHW Code, wherein the statue has made it clear that up to 30 days of leaves can be carried forward and leaves are encashed on demand, death, superannuation, termination and resignation. Now that the erstwhile state law continues to apply to managerial and supervisory employees and the central code all other employees, the overlap in relation to encashment of leaves and carry forward, therefore, must be dealt with care and caution. Employers must incorporate this overlap harmoniously into their leave policy.

- Karnataka Shops and Commercial Establishment Act, 1961 applies to employees in managerial, administrative and supervisory roles drawing wages more than Rs. 18,000. The OSHW code applies to all other employees.

- As per the Karnataka Shops and Commercial Establishment Act, 1961, a maximum of 45 days of leaves can be carried forward and accumulated leaves can be encashed only when employee is terminated or where upon denial of leaves the employee quits.

- Under the OSHW Code, maximum of 30 days of leave can be carried forward. Accumulated leaves are encashed on demand, death, discharge, superannuation, and resignation of the employee.

Overseas Share Swap Structures

Share swaps are a widely used consideration mechanism in cross border transactions where equity, rather than cash, is exchanged between parties. In an overseas share swap, either the shares being transferred or the shares being received (or both) are located outside India. Such structures are commonly used in cross border acquisitions, group reorganisations, holding company formations, and strategic investments.

While overseas share swaps offer commercial flexibility and liquidity conservation, they also raise significant regulatory and tax considerations, especially from an Indian perspective. This article sets out the principal overseas share swap structures used in practice, followed by a structured overview of their tax and regulatory implications.

A. Key Overseas Share Swap Structures

1. Indian Company Acquiring a Foreign Target (Outbound Share Swap)

Mechanics

- Indian company acquires shares of the overseas target by issuing its own shares to foreign shareholders of the Target Company.

- Foreign shareholders of the Target Company receive shares of the Indian company (generally the stake is not very huge)

- No cash consideration is paid.

Commercial rationale

- Overseas expansion without deployment of cash.

- Suitable for strategic acquisitions and operating expansions.

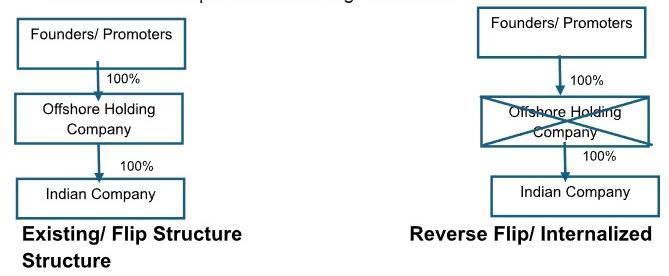

2. Overseas Holding Company Formation (Flip or Inversion Structure)

Mechanics

- New Foreign Hold Co. is incorporated

- Existing shareholders of Indian Company exchange their shares in the Indian company for shares in an offshore HoldCo.

- Indian business continues as an operating subsidiary.

Commercial rationale

- IPO driven restructuring.

- Alignment with foreign venture capital or PE expectations.

- Facilitates overseas capital raising and acquisitions.

3. Foreign Company Acquiring an Indian Company via Share Swap

Mechanics

- Foreign Company purchases the shares of the Indian Target Company from the Indian shareholders and issues its shares to them - Foreign company acquires ownership of the Indian company.

- Indian Company becomes the wholly owned subsidiary of the Foreign Company

Commercial rationale

- Enables Indian promoters to participate in global growth.

- Avoids immediate cash exit.

- Useful where the Acquiring Company is a global listed entity.

B. Regulatory Implications (India-Focused)

- FEMA Considerations

- Permitted under the automatic route if sector is open to FDI, pricing guidelines to be complied with. ODI regulations to be complied with especially with respect to limits of financial commitments.

- Valuation must be conducted by a recognised or registered valuer.

- Mandatory reporting through FC-GPR (issuance of shares), FC-TRS (transfer of shares), Form FC (ODI reporting for investment in foreign entity), as the case may be.

- Sectoral caps and downstream investment rules continue to apply.

- Companies Act, 2013

- Board and shareholder approvals to be obtained.

- Valuation from a registered valuer to be obtained.

- Disclosure and filing obligations apply even in non-cash transactions.

- SEBI Regulations (for Listed Companies)

- Preferential allotment pricing norms apply.

- Shareholder approval by special resolution required.

- Lock-in requirements for issued shares.

- Enhanced disclosure obligations under LODR regulations.

- Income-Tax Implications

- Capital Gains Tax

- Capital gains where there is exchange of Indian shares.

- Consideration to be based on valuation report - Fair market value for the Indian shares transferred. Valuation of Foreign Company shares to be made for the swap

- Long-term or short-term character depends on holding period.

- Tax on Issue of Shares (Section 56)

- Shares must not be issued below fair market value.

- Genuine M&A transactions rely heavily on valuation justification.

- Anti-Avoidance Risks

- GAAR applicability where main purpose is tax avoidance.

- Place of Effective Management (POEM) risks in holding company structures.

- Substance, commercial rationale, and governance location are critical.

For Indian shareholders, a share swap is generally treated as a taxable transfer.

Key points

Where an Indian company issues shares, valuation becomes critical.

Key points

Certain structures may attract enhanced scrutiny.

Key risks

Overseas share swaps are permitted under Indian exchange control laws. Some of the key considerations from tax and regulatory perspective have been provided below:

Key regulatory points

Issuance or transfer of shares through a swap must comply with Indian company law requirements.

Key implications

Where an Indian listed company is involved, securities regulations add another compliance layer.

Key implications

Overseas Tax and Stamp Duty Considerations

Tax outcomes in the foreign jurisdiction depend on local legislation and treaty benefits.

Typical considerations

- Some jurisdictions tax share swaps. Capital gains exemptions may be available subject to anti-abuse rules.

- Stamp duty on share transfers may apply in India and overseas, depending on jurisdiction.

Conclusion

Overseas share swaps are commercially efficient tools that enable cross border acquisitions, restructurings, and global expansion without immediate cash outflow. However, their execution requires careful navigation of Indian exchange control rules, company law requirements, and most critically, capital gains tax exposure.

While regulatory permission for share swaps is broadly available, tax neutrality in India is limited and highly structure-dependent. Consequently, successful implementation requires integrated legal, tax and valuation planning, supported by clear commercial substance.

When designed thoughtfully, overseas share swaps can be powerful enablers of long term value creation; when structured without due care, they can result in significant tax leakage and regulatory risk.

Overseas share swaps are commercially efficient tools that enable cross border acquisitions, restructurings, and global expansion without immediate cash outflow. However, their execution requires careful navigation of Indian exchange control rules, company law requirements, and most critically, capital gains tax exposure.

While regulatory permission for share swaps is broadly available, tax neutrality in India is limited and highly structure dependent. Consequently, successful implementation requires integrated legal, tax and valuation planning, supported by clear commercial substance.

When designed thoughtfully, overseas share swaps can be powerful enablers of long term value creation; when structured without due care, they can result in significant tax leakage and regulatory risk.

Structuring of Intellectual Property (IP) in a Multinational Group

In the modern economy, intangible assets (patents, software, algorithms, trademarks, and trade secrets) generate a significant share of enterprise value. As MNEs scale globally, determining where IP should be housed, and how it should be structured, has become a strategic decision with far reaching tax, regulatory, and operational impacts. The global shift driven by OECD BEPS 2.0, Pillar Two minimum tax, and rising economic substance rules requires that IP ownership reflect real value creation, R&D activity, and management control.

1. Determining the Suitable Jurisdiction for Housing IP

Choosing the right country for IP ownership is no longer about low tax, it is about aligning tax efficiency with substance, R&D nexus, enforcement strength, and treaty access.

- Tax Regime and IP Incentives

- Treaty Network Strength

- Substance and Economic Presence

- IP Protection Environment

Leading IP jurisdictions viz. Ireland, Luxembourg, Netherlands, Singapore, Switzerland, offer low effective tax IP regimes, typically through OECD compliant patent boxes.

Jurisdictions like Netherlands, Luxembourg, and Singapore have expansive treaty networks that reduce withholding taxes on royalty flows, creating efficient income channels for global licensing.

Economic substance (local directors, decision makers etc.) is mandatory in nearly all holding jurisdictions. Tax authorities reject IP entities lacking operational presence.

The US, EU, and Switzerland continue to lead in terms of legal protection, enforcement quality, and IP litigation infrastructure.

2. Common IP Holding Structures Used by Multinational Groups

Below is a brief, tax focused overview of global IP holding structures.

- Centralized IP Holding Company (IP Hold Co)

- IP is owned in a single tax efficient, substance rich jurisdiction

- R&D Entity (located in other jurisdiction) develop and charge cost plus margin to the IP Hold Co.

- IP Hold Co grant IP rights to operating entities in other jurisdictions for royalty.

Tax benefits: Lower effective tax rates, strong treaty networks, and defensible substance and DEPME alignment. GAAR and PPT provisions to be taken care of.

- Regional IP Hubs

- Multinational group establishes multiple IP ownership and development entities, each responsible for a specific region (EU, APAC, Americas)

- Regional Hub Licenses IP to Operating Companies in the Region

Tax Implications: Reduction in cross border royalty withholding tax; TP Requirements to be met, Alignment with BEPS & DEMPE Compliance. GAAR and PPT provisions to be taken care of.

- Licensing and Sublicensing Model

- Ultimate IP Hold Co licenses IP to an intermediate IP Hold Co generally for a royalty

- Intermediate IP Hold Co then sublicenses to local operating entities for a royalty

Tax Implications: Royalties taxed at respective entity level - operating entities taking royalties as deduction. However, important to ensure that intermediate Hold Co has commercial substance (not mere conduit), profits retained in intermediate Hold Co in line with DEPME functions. Withholding taxes can be minimized. GAAR and PPT provisions to be complied with.

- Cost Contribution / Cost Sharing Arrangements

- Group entities jointly fund R&D and co own IP in proportion to the expected future economic benefit

- Instead of royalties, cost sharing payments made to keep contributions aligned with expected benefits (for use of IP made)

Tax Implications: No withholding tax implications, cost contributions claimed as deduction, it is important to align the functions with DEMPE, compliance with BEPS Pillar II provisions required. GAAR and PPT provisions to be taken care of.

3. If a Group Currently Holds IP in India: Options for Migration or Internal Structuring

Many MNEs and Indian origin companies currently hold core IP in India due to historic development teams. With globalization, there may be a need to shift ownership to a globally efficient IP jurisdiction Below are a few restructuring options which could be considered for shifting the IP:

- Option 1: Direct IP Transfer to IP Hold Co

A transfer of IP from India to an overseas IP Hold Co.

Mechanism

- Transfer executed via transfer deed.

- IP Hold Co pays arm’s length purchase price.

Tax/Regulatory Implications

- Transfer triggers capital gains in India; valuation required. Withholding tax requirements

- FEMA compliance is mandatory for transfer of intangible assets.

- GST impact to be considered

- Option 2: Hive Off of IP into a Newly Created Indian Entity Followed by Share Transfer

- Transfer IP (undertaking) into a dedicated India SPV (can be done as a demerger or slump sale)

- Transfer shares of that SPV to the IP Hold Co

- Capital gains on hive off of IP (tax benefits under demerger, tax cost can be reduced under slump sale)

- Capital gains on share transfers. Can be minimized to a greater extent. Valuation requirements to be complied with – Withholding tax requirements to be complied with

- FEMA implications (including valuation requirements) on share transfer to be taken care of.

- Company Law provisions to be complied with

- Option 3: Cross-Border Merger

- Capital gains impact on Indian Co and shareholders to be taken care of

- Compliance with FEMA (Cross Border Merger) Regulations, 2018 to be done – FEMA Odi regulations to be complied with if Indian shareholders receive shares of IP Hold Co

- Company law provisions relating to outbound merger to be complied with

- Valuation requirements under FEMA and Company Law to be complied with

Mechanism

Tax/Regulatory Implications

The Indian company holding IP merges into a IP Hold Co entity outside India, shifting IP ownership.

Tax/Regulatory Implications

Determining where to house IP and how to structure it, is one of the most consequential decisions for any multinational group. The ideal jurisdiction will combine tax efficiency, strong IP protection, substance-based incentives, and treaty network benefits.

Ultimately, the optimal structure is one that marries commercial logic with regulatory defensibility in the BEPS driven era.

Impact of Illiquidity & Control Discounts on Valuation — A Valuer's Perspective

As a valuer, arriving at the "Fair" value of a business is not just about crunching numbers. Two major adjustments that come up almost every time we value a private company are:

- Illiquidity Discounts, and

- Control Discounts

These are not just academic or a theoretical concept. They are the assumptions through which a valuer blends practical ground realities with the valuation and getting them wrong can significantly impact the final valuation.

What Does a Valuer Mean by Illiquidity Discounts?

When we value a listed company, the stock price is available in real time and the holder of the share has the liberty to buy and sell the share at his will. But when it comes to an unlisted company, ease of having a readily available benchmark does not exist.

Finding a buyer for an unlisted share can take a long time. Even when a buyer is found, the deal pricing completely depends on the commercial negotiations. This inability to exit quickly and at fair value is what we call illiquidity, and to account for it, we apply an illiquidity discount to the value of the company.

In India, this is a judgment call valuers face frequently, given the large base of unlisted companies across sectors.

What Does a Valuer Mean by Control Discounts?

Control Discounts, in pure valuation language, refers to the ability of a shareholder to influence what happens inside the company.

A shareholder holding 60% can push through decisions, whereas a shareholder holding 10% in the company, in most cases, cannot. This difference in power is real, and it affects valuation.

In India, this matters even more considering the fact that most businesses are promoter-driven, with decision-making tightly held at the top. Minority shareholders often have little say, even if investor agreements provide some protective rights.

How These Discounts are applied in Practice

Here is how the math actually works in a typical valuation assignment: Suppose a company is valued at ₹50 crore using a standard method like Discounted Cash Flow. At face value, that is the valuation number we arrive at. But this is the value before we account for ground realities.

We then ask two questions:

- Can this stake be sold easily? → No. It is an unlisted company with no active buyer base.

- Does the ownership carry any meaningful control? → No. It is a passive minority holding.

We then apply, say, a 10% control discount and a 10% illiquidity discount:

- After illiquidity and control discount: ₹50 crore × 80% = ₹40 crore

A company that appeared worth ₹50 crore on paper is now valued at ₹40 crore — a reduction of 20% straightaway. This is what makes these discounts so significant. A valuation without these adjustments is simply incomplete and this is where the valuer's judgment goes beyond the spreadsheet.

What Influences the Quantum of these Discounts?

There is no set precedent for a valuer to decide upon these percentages, the quantum of these discounts depends on several factors:

- Shareholder agreements - Does the investor have tag-along rights, exit clauses, or a right of first refusal?

- Company size and reputation - A well-known private company with strong fundamentals attracts more buyers, which reduces illiquidity.

- Industry and growth potential - High-growth sectors attract strategic buyers, improving exit prospects.

- Past transaction benchmarks - Comparable deals in similar businesses give a reference point.

International studies provide a range, but it generally boils down to valuer’s judgement on the industry and other company specific prospects, especially given India's unique ownership structures and still-maturing secondary markets.

Why This Matters

Ignoring these discounts or applying them mechanically without thought often leads to valuations that do not reflect reality. Overstating a valuation can mislead investors, create disputes, or result in regulatory scrutiny, especially since SEBI and income tax regulations in India increasingly require proper justification for valuation assumptions and adjustments.

While valuation a private company, ask two simple questions - Can this be sold easily? and Does this give the holder any real power? If either answer is no, a discount is warranted. The size of that discount is where professional judgment, experience, and market knowledge come in.

Managing global data flows: legal rules governing transfers from India

India is burgeoning as one of the Global Capabilities Centre to Multinational Companies. Given this, it is only obvious that there are significant data exchanges between companies to conduct their operations. That is to say that India is emerging as data processors, owing to which MNC will be subjected to obligations under Indian Law as data fiduciaries. In an age where personal data is the “modern day gold”, and where regulations surrounding “personal data” is only increasing by the day and is nerve-racking to companies across the globe, cross-border data transfer is no longer a compliance checkbox, but a strategic imperative for sustainable growth. This article aims to simplify and structure the regulations related to cross-border transfer of personal data under the Indian laws.

What is transfer?

First thing one needs to understand is the term “Transfer”. It is pertinent to note that the Indian data protection framework falls short in defining this term. However, as per Oxford dictionary this refers to “move from one place to another”. Hence, it can be interpreted widely. From a general data practice perspective transfer can be effected in the following ways -

- Data sent to the transferee for storage in the latter’s country (Data centers located in transferee country)

- Data is stored in transferor country but is virtually accessed by the transferee.

Old Regime

The Indian data protection regime is marking a significant transition from the Information Technology (Reasonable security practices and procedures and sensitive personal data or Information) Rules, 2011 (“SPDI Rules”) under the Information Technology Act, 2000 (“IT Act”) to the Digital Personal Data Protection Act, 2023 (“DPDPA”) by May 2027.

The SPDI Rules as it is the first data protection law in India is primitive. While SPDI Rules per se does not prohibit cross border transfer of sensitive personal data, Rule 7 allows it provided the following are complied with –

- Data protection laws of the other country must be in the same level as that of India.

- Transfer is allowed only if it is necessary for the performance of the contract between Company and person.

- Companies must obtain consent for transfer of information to another country.

Moreover, “sensitive personal information” is finite list of personal information relating to –

- password;

- financial information such as Bank account or credit card or debit card or other payment instrument details ;

- physical, physiological and mental health condition;

- sexual orientation;

- medical records and history;

- Biometric information;

- any detail relating to the above clauses as provided to body corporate for providing service; and

- any of the information received under above clauses by body corporate for processing, stored or processed under lawful contract or otherwise.

While, not all personal information is sensitive personal information, all sensitive personal information is personal information. That is to say that Rule 7 of SPDI Rules shall only apply when there is transfer of sensitive personal data. However, personal data such as name, address, social security numbers, employment records can be transferred cross-border without any restriction until May 2027.

New regime

The implementation of DPDPA by May 2027 ushers in a new era on the protection of personal data. The legislation adopts an expansive and far-reaching approach to its applicability, as set out below:

- Unlike the erstwhile SPDI rules, the DPDPA defines personal data to include any and all information through which an individual is identifiable.

- The DPDPA primarily concerns itself with the processing of personal data within the territory of India. It does not differentiate between the data of Indian citizens and non-Indian citizens, be it digitized or not, or be it processed by Indian entity or not. As long as processing of personal data happens within Indian borders, the DPDPA is applicable.

- It is trite to note that the DPDPA is indifferent to the location from which personal data is accessed or controlled. As long as the processing (normalization, deidentification and data analysis) is carried out within India, the obligations under DPDPA extends to Data Fiduciary, even if such data fiduciary is situated outside India.

With regard to restrictions on transfer of data, section 16 of the DPDPA empowers the Central Government of India to blacklist certain countries to whom data fiduciaries are restricted to transfer data for processing. However, it does not prohibit the application of any sector specific law restricting transfer of personal data. In the absence of any sector specific legislation, MNC’s may, for the time being, operate with relative certainty in transferring data to and from India, as –

- The Central Government is yet to roll out list of blacklisted countries and regulations/rules restricting transfer of personal data to other countries.

- Moreover, section 16 of the DPDPA only restricts a Data Fiduciary to transfer the personal data for further processing to another country. However, alternatively, the law does not restrict a Data Processor from transferring the data to any other country be it even for storage.

Conclusion:

From the above discussion, it is clear that currently in India transfer of personal data across borders is permitted provided certain compliances are met (i.e., data protection laws of countries are equal and comparable, transfer should be allowed if necessary for performance of contract and obtaining of consent). That being said, it is pertinent to note that Personal Data Protection is an evolving jurisprudence. In India, data privacy/right to privacy is viewed as a constitutional right of Right to Life under Article 21 of the Constitution of India, 1950. Furthermore, the primary objective of the DPDPA is to “recognize the right to individuals to protect their personal data”. Recently, the Supreme Court of India, while hearing an appeal from Meta Platforms Inc. (WhatsApp) prohibited Meta from transferring personal data of its Indian users to other Meta Platform Entities on the grounds of constitutional right of privacy. There is growing importance to data security and data privacy in India. Given that the DPDPA has cross border application, on how judiciary or legislature will view compliance under this only time will tell.

- Up until May 2027, India’s data protection legislation is fragmented into two parts, increasing the compliance checkbox for multinational corporations.

- While post complete implementation of the DPDPA, nothing is etched in stone to prohibit data fiduciary or data processor from transferring data out of the Indian territory. However, regulatory uncertainty and judicial activism might signal a restrictive future.

Market Over Mandate: Decoding the RBI's Overhauled ECB Framework

The revised External Commercial Borrowing framework marks more than a routine regulatory update; it reflects a deliberate shift in how the RBI conceptualises and manages external debt.

This article intends to examine the underlying rationale for this shift, exploring why the RBI chose to redraw the contours of the ECB regime and what this change signals about the evolving philosophy of external debt regulation in India.

Decoupling FDI linkages – Who gets through the door now?

- The earlier framework permitted only FDI-eligible entities to avail an ECB.

- However, the FDI linkage placed high emphasis on ownership, control and sectoral sensitivities for a pure-debt transaction where these are largely peripheral.

- Removal of this linkage would now expand access of offshore debt capital to a lot of credit-worthy but not FDI eligible entities, which can now avail ECBs based on their legal incorporation and financial strength.

Who Can Lend Now—and What That Signals

- Under the earlier regime, recognised lenders were limited to specific categories of institutions that met prescribed regulatory and jurisdictional criteria.

- The new framework moves away from this prescriptive listing and permits ECBs to be raised from any person resident outside India, including foreign branches and IFSC units of entities engaged in regulated lending activity.

- This change signals the RBI’s decision to rely on market discipline and lender due diligence rather than regulatory screening and acknowledges the diversity of global credit markets which allows Indian borrowers to access a wider spectrum of funding sources.

Rethinking Borrowing Limits

- ECB access was previously constrained by a fixed cap, with borrowers permitted to raise up to USD 750 million per financial year under the automatic route.

- This approach imposed a uniform ceiling, largely indifferent to the borrower’s balance sheet strength or aggregate leverage.

- In the revised framework, borrowers may now raise ECBs up to the higher of

- USD 1 billion in outstanding ECBs

- total outstanding borrowings; up to 300% of net worth, based on the latest audited balance sheet.

- In doing so, the RBI has shifted from a quantitative cap to a model that allows access to offshore debt in proportion to a borrower’s capital base.

Untangling Purpose, Tenor and Cost

- Under the earlier ECB framework, end use restrictions were not merely about how borrowed funds could be deployed. They in turn affected several other factors such as tenor and cost of borrowing.

- The same borrower raising the same amount could face different minimum maturities solely because of the stated end use. This often-pushed borrowers to structure transactions backwards by shaping end use narratives to secure a more favourable tenor rather than aligning borrowings with business needs.

- End use also indirectly constrained pricing and refinancing, as longer mandated maturities increased interest rate and credit risk for lenders, while a fixed all in cost ceiling prevented those risks from being priced appropriately.

- The revised ECB framework marks a significant shift from the earlier approach by delinking end use from maturity and pricing.

- Pricing is now market determined, and the minimum average maturity period has been standardised at 3 years. A limited flexibility is retained for manufacturing entities, which may access ECBs with a defined cap for a shorter tenure between 1 and 3 years.

- Further, end-use regulation is also anchored around a clearly defined negative list, with proceeds prohibited from being used for:

- Chit funds and Nidhi Companies

- Real estate business and construction of farmhouses

- Agricultural and animal husbandry activities

- Plantation activities (except tea, coffee, rubber, cardamom, palm and olive oil)

- Trading in Transferable Development Rights

- Investment in listed and unlisted securities (Except for corporate restructuring transactions)

- Repayment of INR loans classified as NPAs

- On lending for prohibited activities

Simplifying Reporting Requirements

- On the reporting front, the revised framework introduces a significant shift from monthly reporting to an event based regime.

- Form ECB 2 is now required to be filed only upon the occurrence of specified events - namely, a change in the outstanding principal amount (whether by way of further drawdown or repayment) or the payment of interest.

- This eliminates the requirement for routine monthly filings in periods where there is no movement in principal or interest.

- The move simplifies and reduces the compliance burden for borrowers, particularly those who were earlier required to file repeated returns despite having fully no draw down or repayment of the Borrowing.

By moving from a model rooted in entry restrictions and policy linkages to one based on prudential safeguards, market discipline, and structural oversight, the RBI’s revised ECB framework seeks to redefine how offshore capital is accessed and regulated.

As the ECB framework shifts, authorised dealer (AD) banks emerge as the critical fulcrum of the new regulatory compact. With expanded access, market determined pricing, and simplified structural rules, much of the RBI’s oversight is now channelled through AD banks’ due diligence, judgment, and monitoring functions. They are no longer merely intermediaries, but active risk filters in ensuring that flexibility is exercised within the framework’s prudential boundaries.

Designing Optimal Holding and Funding Structures for Modern Businesses

As businesses expand across borders, enter new markets, and diversify ownership, the choice of holding and funding structures becomes a central strategic decision. The right structure improves tax efficiency, safeguards assets, supports investor expectations, and enhances the ability to raise capital.

This article examines the principles, options, and considerations involved in designing optimal holding and funding structures - for both multinational operating groups and private capital–backed ventures.

1. The Role and Purpose of Holding Structures

A Holding company is a Company in which the investments, subsidiaries, intangible assets, or business operations are consolidated. The holding structure influences taxation, control, consolidation of cash flows and the company’s ability to reorganize.

Key objectives of a well-structured holding company:

- Tax Efficiency: Access to treaty networks, participation exemptions, low withholding taxes, and efficient capital gains regimes.

- Risk Isolation: Ring fencing business units to protect core assets from operational liabilities.

- Financing Flexibility: Centralizing treasury management, leveraging debt pooling, and consolidating borrowing capacity.

- Ease of Exit: Facilitating share sales, carve-outs, IPOs, or partial divestments.

- Governance and Control: Providing clear oversight and a robust platform for investor protections.

2. Choosing the Right Jurisdiction for the Holding Company

Selecting a holding jurisdiction is a multi-factor decision. Commonly evaluated options include Singapore, the Netherlands, Luxembourg, the UAE, and increasingly onshore hubs like India’s GIFT City for India-centric groups. The choice depends on:

- Tax treaty access

- Reduced withholding tax on dividends, interest, and royalties

- Protection from capital gains taxation on disposals

- Clear relief from double taxation

- Beneficial definitions for permanent establishment (PE) and valuation

- Domestic tax environment

- Corporate tax rate and exemptions

- Participation exemption for dividends/capital gains

- No or minimal capital duty or transfer taxes

- Availability of tax rulings for certainty

- Economic and substance requirements

- The holding entity must demonstrate real substance

- Board meetings, key personnel, local expenditure, and documentation must align with operational reality

- Regulatory ease and investor familiarity

A holding jurisdiction must ideally provide:

Key aspects include

Increasing global scrutiny means:

A jurisdiction’s reputation, predictability, and access to sophisticated financial services matter - particularly for PE/VC-backed companies with multi-jurisdictional shareholders.

3. Optimal Funding Structures Within the Group

Designing an optimal funding structure is a critical component of business strategy. It determines how a company finances its growth, manages risk, minimizes tax leakage, and maintains financial flexibility. An effective structure balances equity, debt, and hybrid instruments to achieve long-term stability while meeting investor expectations.

- Objectives of an Optimal Funding Structure

- Minimize cost of capital while maintaining adequate liquidity

- Ensure tax efficiency (e.g., interest deductibility)

- Provide flexibility for future raises and acquisitions

- Align with regulatory requirements (FEMA, FDI rules, thin capitalization norms)

- Balance leverage vs. risk to maintain creditworthiness

- Protect shareholder value and avoid unnecessary dilution

- Components of Funding Structure

- Equity Funding

- No repayment obligation

- Strengthens balance sheet and borrowing capacity

- Suitable for high-growth, cash-burning phases

- Dilution of ownership

- Dividends are not tax deductible

- Valuation pressures during downturns

- Debt Funding

- Interest is tax deductible, reducing effective financing cost

- No dilution

- Predictable repayment schedules

- Excessive leverage increases financial risk

- Thincapitalization rules can restrict interest deductions

- Withholding tax may apply on cross-border interest

- Hybrid Instruments

- Flexibility in structuring return (interest, dividend, conversion)

- Tax-efficient alternatives to straight equity

- Useful in private equity structures where multiple investor classes exist

An optimal funding structure aims to:

Equity represents permanent capital contributed by owners.

Pros:

Cons:

Equity is most efficient when funding innovation, technology development, and strategic acquisitions.

Debt provides leverage and tax efficiency.

Pros:

Cons:

Debt is ideal for stable, cash-generating businesses with predictable earnings.

These combine features of equity and debt (CCD/ OCDs, CCPS/ OCPS)

Benefits:

Hybrids work well when balancing control, taxation, and capital needs.

4. Key Considerations in Designing the Structure

- Tax Efficiency

- Maximize interest deduction while staying within thin-cap rules

- Evaluate withholding taxes on interest vs dividends

- Optimize cross-border flows through treaty-favorable jurisdictions

- Regulatory Compliance

- FEMA/FDI rules govern pricing, repayment, conversions

- External Commercial Borrowings (ECBs) require adherence to end use restrictions and maturity norms

- Equity instruments must follow sectoral caps and reporting requirements

- Cash Flow & Repayment Capacity

- Operating cashflows

- Expected project timelines

- Ability to service debt without liquidity stress

- Investor Expectations

- Private equity funds prefer convertible or structured instruments

- Promoters typically seek minimum dilution

- Lenders prefer senior secured instruments

For India-related structures:

Funding must align with:

A balanced structure aligns the interests of all stakeholders.

5. Tax Optimization Through Strategic Structuring

- Minimizing Withholding Tax Leakage

- Inbound dividends

- Royalty payments

- Interest flows

- Intercompany service charges

- Capital Gains Optimization

- Use jurisdictions offering capital gains exemptions

- Avoid countries with “indirect transfer” rules without treaty protection

- Consider pre-exit reorganizations to optimize tax outcomes

- Transfer Pricing and Substance

Selecting jurisdictions with beneficial treaty networks can significantly reduce WHT on:

A tax-optimized structure considers both the source and residence country rules, aligning ownership layers accordingly.

A top consideration for investors is the tax cost of exit. Efficient structures:

For private equity funds, ensuring capital gains fall in treaty-protected jurisdictions can materially improve net IRR.

Intercompany transactions - royalties, management fees, financing, IP transfers - must comply with transfer pricing rules. Substantial documentation, real economic substance, and DEMPE alignment (for IP) are essential to avoid disputes.

6. Managing Regulatory Compliance: FEMA, BEPS, GAAR, and Governance

For India-inbound or India-outbound structures, FEMA considerations are central:

- Pricing guidelines/ Sectoral caps

- Reporting obligations (FC-GPR/FC-TRS, ODI forms)

- Restrictions on round-tripping

Globally, BEPS and GAAR require that tax outcomes reflect genuine business substance and commercial rationale.

Governance must be designed to withstand:

- Transfer pricing audits

- Anti-avoidance reviews

Optimal holding and funding structures emerge from a thoughtful balance of tax efficiency, regulatory compliance, investor expectations, business strategy, and geographic exposure. In a world governed by anti-avoidance rules and substance requirements, the best structures are those rooted in commercial reality, supported by clear documentation, and aligned with long-term operational plans.